Join a Credit Union in Wyoming: Personalized Financial Providers for You

Wiki Article

The Ultimate Guide to Recognizing Cooperative Credit Union

Cooperative credit union stand as one-of-a-kind financial entities, rooted in concepts of mutual assistance and member-driven procedures. Past their fundamental values, comprehending the detailed workings of credit rating unions includes a much deeper exploration. Untangling the complexities of subscription qualification, the evolution of services supplied, and the distinct advantages they bring calls for a comprehensive evaluation. As we browse via the complexities of credit unions, an insightful journey awaits to drop light on these member-focused establishments and just how they vary from traditional banks.What Are Credit History Unions?

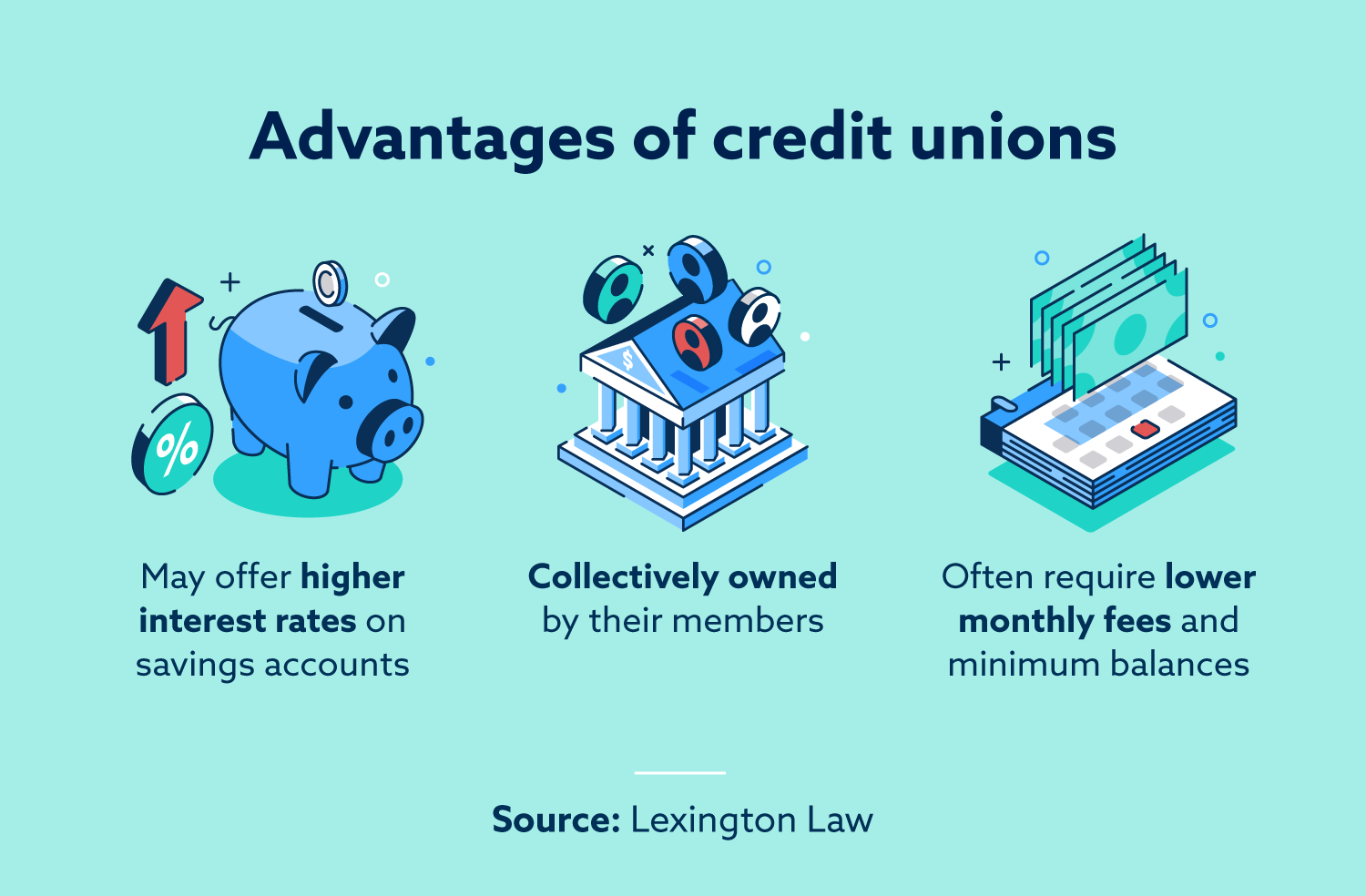

Credit score unions are member-owned banks that supply a series of banking services to their participants. Unlike traditional banks, lending institution run as not-for-profit organizations, suggesting their primary emphasis is on offering their participants instead of taking full advantage of revenues. Participants of a cooperative credit union commonly share an usual bond, such as functioning for the same company, belonging to the exact same area, or being component of the very same organization.One of the key advantages of credit rating unions is that they usually use greater rates of interest on interest-bearing accounts and reduced rate of interest on fundings contrasted to banks. This is because credit rating unions are structured to benefit their participants straight, allowing them to pass on their profits in the type of better prices and less costs. Additionally, credit score unions are understood for their personalized client service, as they focus on building partnerships with their members to understand their one-of-a-kind economic demands and goals.

History and Evolution of Cooperative Credit Union

The origins of member-owned financial cooperatives, recognized today as cooperative credit union, trace back to a time when neighborhoods looked for choices to standard financial establishments. The concept of lending institution originated in the 19th century in Europe, with Friedrich Wilhelm Raiffeisen commonly attributed as the leader of the participating banking activity (Credit Unions Cheyenne WY). Raiffeisen founded the first identified lending institution in Germany in the mid-1800s, stressing community support and self-help principles

The evolution of cooperative credit union continued in The United States and Canada, where Alphonse Desjardins developed the first credit scores union in Canada in 1900. Shortly after, in 1909, the very first U.S. cooperative credit union was developed in New Hampshire by a group of Franco-American immigrants. These very early credit unions operated the basic principles of common support, democratic control, and participant possession.

Over time, credit unions have grown in appeal worldwide because of their not-for-profit structure, concentrate on offering participants, and offering affordable financial items and solutions. Today, cooperative credit union play an essential duty in the financial sector, offering community-oriented and obtainable banking alternatives for people and businesses alike.

Subscription and Eligibility Standards

Subscription at a lending institution is typically limited to people fulfilling details eligibility standards based on the establishment's beginning concepts and governing requirements. These criteria often consist of elements such as geographic place, work status, subscription in specific companies, or association with specific teams (Wyoming Federal Credit Union). Credit scores unions are recognized for their community-oriented strategy, which is shown in their subscription requirements. Some credit history unions may only offer people who work or live in a particular location, while others may be customized to workers of a certain business or participants of a specific association.Furthermore, cooperative credit union are structured as not-for-profit organizations, meaning that their key objective is to serve their participants as opposed to produce profits for investors. This emphasis on participant service often converts into more individualized interest, lower charges, and affordable passion rates on financial savings and loans accounts. By satisfying the qualification criteria and ending up being a member of a credit scores union, people can access a variety of economic services and products customized to their specific needs.

Solutions and Products Supplied

One of the vital aspects that sets credit scores unions apart is the varied variety of financial solutions and products they supply to their participants. Credit scores unions generally give standard banking solutions such as Wyoming Credit Union savings and inspecting accounts, finances, and credit score cards.

Furthermore, cooperative credit union usually offer convenient online and mobile financial choices for participants to conveniently handle their finances. They may supply benefits such as common branching, allowing members to access their accounts at various other lending institution throughout the country. Some credit report unions also give insurance items like life, auto, and home insurance coverage to aid members safeguard their possessions and enjoyed ones.

Along with financial services, lending institution frequently take part in neighborhood outreach programs and economic education and learning initiatives to support their members in accomplishing their monetary goals.

Benefits of Financial With Lending Institution

When considering banks, checking out the advantages of banking with lending institution discloses one-of-a-kind advantages for participants looking for individualized solution and affordable prices. One substantial benefit of lending institution is their concentrate on personalized client service. Unlike huge financial institutions, lending institution are member-owned and focus on structure strong relationships with their members. This means that lending institution staff frequently have a deeper understanding of their participants' monetary requirements and can provide tailored services to assist them accomplish their goals. Additionally, lending institution are recognized for supplying affordable rates of interest on financial savings and financings accounts. Due to the fact that they are not-for-profit organizations, credit report unions can commonly supply reduced financing rates, higher financial savings rates, and reduced charges compared to standard banks. This can cause considerable price financial savings for members with time. Generally, banking with a debt union can supply a much more personalized, cost-efficient, and member-centric monetary experience.Conclusion

Debt unions are member-owned economic institutions that offer an array of banking services to their participants. The principle of credit history unions originated in the 19th century in Europe, with Friedrich Wilhelm Raiffeisen typically attributed as the leader of the participating financial movement.The evolution of credit report unions proceeded in North America, where Alphonse Desjardins developed the first credit history union in Canada in 1900. Credit score unions typically provide conventional banking solutions such as savings and examining accounts, car loans, and credit cards.When considering financial institutions, exploring the benefits of banking with credit report unions reveals special benefits for members seeking customized solution and competitive rates.

Report this wiki page